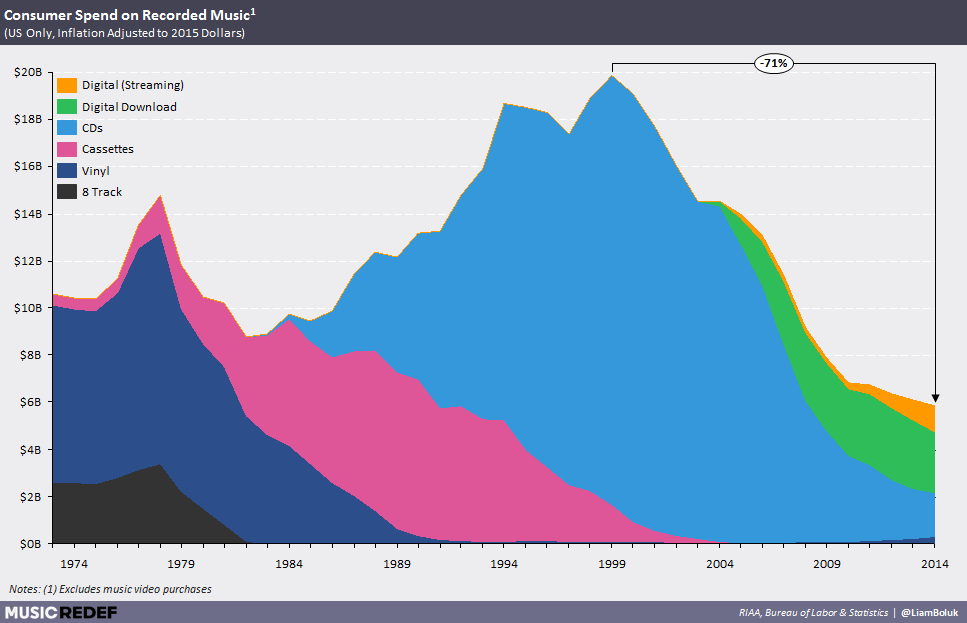

“Music is art, and art is important and rare,” Taylor Swift wrote in the Wall Street Journal in July of 2014 (months before pulling her catalogue from Spotify), “Important, rare things are valuable. Valuable things should be paid for.” Yet of all the mass media, music is perhaps the least rare, most substitutable and in many instances, the most imitable (just ask Max Martin or Dr. Luke). For nearly half a century, however, the major labels (and therefore their artists) have held a de facto monopoly on the music industry and its output – all by controlling distribution. The costs of recording, producing, distributing and marketing a studio album – not to mention getting a track played on national radio stations – were so significant that few could do so at scale without the major labels. Furthermore, the major labels had scale-related incentives that limited the number of artists they were willing to support. As a result, the supply of both artists and music was fundamentally constrained.

Digital distribution ended this artificial scarcity, and with it the idea that music – even great music – was scarce. Spotify, for example, counts more than 30 million tracks, each available anywhere and anytime. Because of this, music lovers can now listen to a much greater variety of music – not just the few albums they’ve bought or what’s on locally programmed radio (which is heavily influenced by the major labels, too). This competition has inevitable economic consequences: prices go down and average units sold per album, track and artist drop. This is particularly true for online streaming. Though every music listener has favorite artists, consumption of music tends to be more passive and voluminous than any other media category. The average Spotify user, for example, listens to more than 1,300 tracks per month. When consumption is that great, the value of any one stream becomes slight. The economics bear this out: if we focus exclusively on Spotify paid subscribers ($9.99/month), the implied value of any one stream was $0.0076 in Q1 of 2015.

Liam Boluk

Great overview of the music industry, covering everything from the status quo a decade ago to the major shifts in consumption and distribution the business is experiencing today and how it will change the future of music.

But in the second half the author starts contradicting himself: you can’t praise the increased competition on the market, the greater selection available for consumers, lament the convoluted methods labels use to calculate artist royalties, and then turn around and demand that Spotify severely restricts its free service in order to push subscribers to the paid service! First of all, there are many other streaming providers – not to mention YouTube – so fixating on Spotify’s business model cannot ‘fix’ the music industry as a whole. Secondly, increasing friction for free users will simply make them turn to other alternatives, even go back to pirating. I think streaming will continue to grow because it’s a better model for customers, and people need to be encouraged to sign up and discover the benefits, not be constantly reminded of the limitation of the free plan. The bigger issue are the monolithic labels, their outdated contracts and increasing control over streaming providers, allowing them to capture most of the streaming profits.

Post a Comment